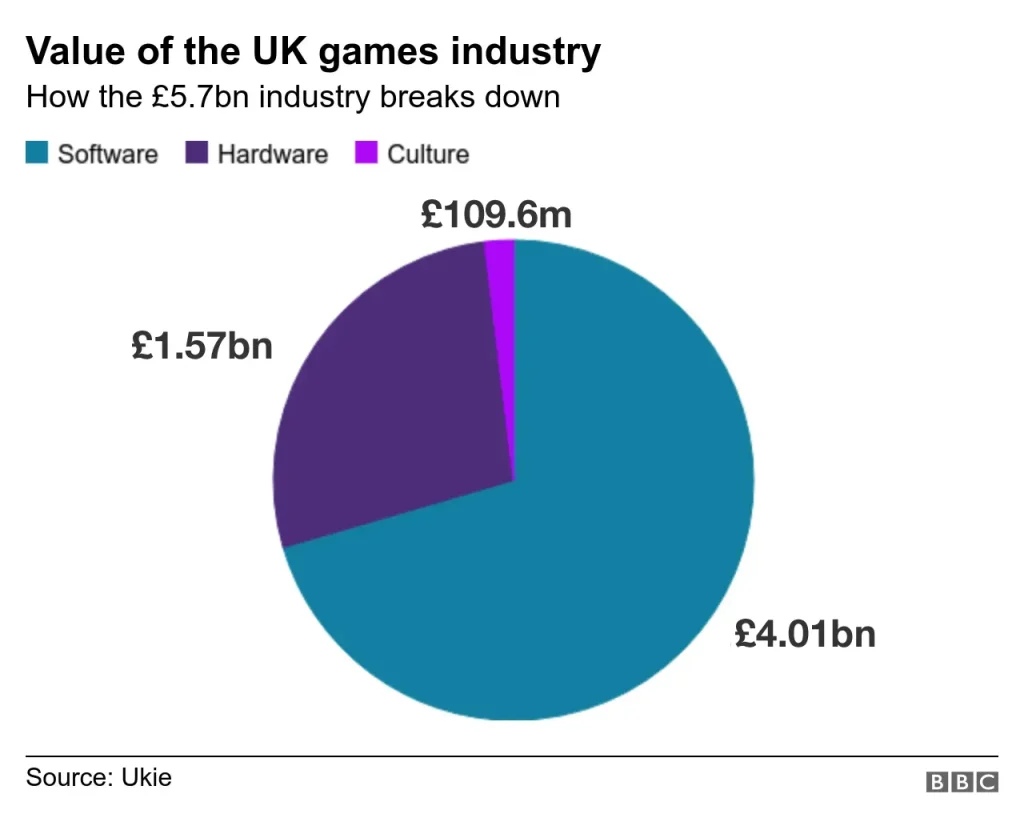

UK video games market growth 2025 is reshaping Britain’s entertainment economy as households spent £5.4 billion on video games in 2025, according to ERA data drawn from NielsenIQ, GfK Entertainment, Omdia and GSD/IFSE, underscoring a year of robust expansion across platforms and sectors. UK video game revenue 2025 rose 7.4% year on year, underscoring the breadth of the market’s turnaround and the durability of consumer demand across physical and digital channels, with retailers reporting stronger performances in bundles, subscriptions, and diverse price promotions that supported overall growth. The mobile game revenue UK 2025 surged 8.8%, lifting mobile revenues to £1.88 billion and illustrating how mobile formats drive most of the growth, supported by popular free-to-play features, in-app purchases, and cross-platform play that broaden the audience. Digital game sales UK 2025 climbed to £5 billion, up 8% year-on-year, reinforcing the shift toward downloads and online access while boxed and physical sales contracted modestly and the proportion of revenue from digital channels continued to outpace traditional formats. ERA UK games data 2025 highlights that ownership remains a priority for many consumers, with boxed sales representing around 5% of total revenue and digital and downloadable content expanding as publishers invest in evergreen franchises and new IP to sustain momentum into 2026.

More broadly, this trend is reflected in terms like the British interactive entertainment market and the UK games ecosystem, which point to a broader shift toward digital distribution, downloadable content, and subscription models that complement traditional ownership. In this frame, the market resembles a resilient media sector, with publishers and retailers adapting to evolving consumer preferences, platform dynamics, and cross-platform opportunities that keep demand resilient into 2026. The second layer of the narrative emphasizes the diverse mix of formats—console and PC downloads, mobile hits, and indie titles—that together drive growth while reinforcing the importance of robust data sources for strategy and forecasting. In sum, the British gaming landscape continues to blend ownership with access, leveraging IP, live services, and data-driven decisions to sustain momentum across the diverse spectrum of consoles, devices, and digital storefronts.

UK video games market growth 2025: drivers and outcomes

In 2025, ERA UK consumers spent £5.4 billion on video games, with data from NielsenIQ/GfK Entertainment, Omdia and GSD/IFSE cited by ERA showing a 7.4% year‑on‑year rise. This marks the strongest growth for the UK games sector since the 2020 pandemic spike, underscoring a sustained rebound as the market adapts to new formats and distribution channels.

The key driver behind UK video games market growth 2025 was mobile titles, which grew 8.8% to £1.88 billion and represented 35.5% of total games revenue. Digital sales surged as part of the same trend, with boxed sales and physical distribution shrinking in relative importance, while the overarching trend points to a resilient, innovation‑driven market that ERA and its partners expect to sustain into 2026.

UK video game revenue 2025 breakdown: mobile, console, and digital

The 2025 revenue mix shows mobile driving the rebound, with an 8.8% increase contributing to £1.88 billion of that year’s total. Digital game sales UK 2025 also roles prominently, delivering £5 billion in revenue as digital channels become the dominant route for many players.

Console game downloads rose notably, delivering about $857.6 million, while physical boxed sales slipped to £318.8 million. Overall, boxed sales represented around 5% of total UK games revenue for 2025, highlighting the tug between ownership‑driven purchases and ongoing digital access models in ERA UK games data 2025.

Mobile game revenue UK 2025: leading the rise in UK gaming

Mobile game revenue UK 2025 stood out as the primary growth engine, with the mobile segment contributing £1.88 billion of the year’s revenue and a broad share of total spend. The 35.5% share of all games revenue underscores how mobile titles captured consumer attention and spending across the year.

This momentum reinforces the central role of mobile in the UK video games market growth 2025, as consumers increasingly favor on‑the‑go experiences and in‑app purchases. The sustained rise in mobile revenue aligns with ongoing innovation in mobile formats and monetisation strategies, as reflected in ERA UK data and subsequent market commentary.

Digital game sales UK 2025: resilience and expansion

Digital game sales UK 2025 demonstrated resilience with £5 billion in revenue, up 8% year on year. The shift toward digital format reflects consumer preference for instant access, updates and cross‑device play, reinforcing the structural change toward digital channels within the UK games market growth 2025.

Digital channels continued to expand despite some declines in boxed and physical formats. This growth has helped sustain overall revenue while enabling publishers and retailers to pursue new licensing, distribution and streaming aligned experiences, as highlighted by the ERA UK games data 2025 analysis.

ERA UK games data 2025: source, methodology, and key takeaways

ERA’s UK games data for 2025 draws on measurements from NielsenIQ/GfK Entertainment, Omdia and GSD/IFSE, with ERA synthesising these inputs to present a cohesive view of consumer spending and format mix. The data emphasise the importance of ownership vs access in shaping revenue trends across the year.

Key takeaways include a 45% share of game revenue from direct purchases rather than subscriptions, a contrast with music (16.6%) and video (7.2%). The period also shows GDP growth of 12% since 2016 while games revenue has risen by 86%, illustrating the sector’s rapid expansion within the UK economy as recorded in ERA UK data 2025.

Physical games vs boxed sales in 2025: a continuing decline

Physical sales dipped by 1% to £318.8 million in 2025, with boxed sales representing about 5% of total UK games revenue. This aligns with broader consumer migration toward digital downloads and streaming, underscoring a shift in the retail mix toward digitally delivered experiences.

The decline in boxed sales contrasts with digital growth, reinforcing the enduring trend of digital game sales UK 2025 as consumers value immediacy and ownership through downloads, while publishers optimise distribution through digital storefronts and direct‑to‑consumer channels.

Console game downloads rise in 2025: growth within a shifting market

Console game downloads rose 11.5% year on year, generating approximately $857.6 million for the period. The strength in console downloads demonstrates how physical‑to‑digital transition and cross‑platform releases can support substantial revenue growth even as the overall market becomes more digital.

This growth in console downloads sits alongside mobile strength and digital sales, contributing to a diversified revenue base for UK players. It also reflects consumers’ willingness to purchase digital versions of major titles, reinforcing insights from ERA UK games data 2025 about format mix and consumer preferences.

Ownership versus access: ERA’s perspective on spending in games

ERA highlights that 45% of game revenue came from consumers buying games outright rather than subscribing, illustrating a persistent preference for ownership in the UK market. This ownership bias stands in contrast to other entertainment sectors and remains a defining feature of the UK games economy in 2025.

The ownership over access dynamic supports a robust boxed and digital ownership market, while subscriptions trend at lower percentages in comparison with music and video. The nuanced mix contributes to the overall UK video games market growth 2025 and informs future pricing and monetisation strategies.

UK entertainment sector: games as a growth engine in 2025

When viewed within the broader UK entertainment category, games contributed to a total spend of £13.3 billion in 2025, up 7.1% year on year. This positions games as a major growth engine within the UK’s entertainment landscape and reinforces the contribution of the ERA UK data to understanding sector dynamics.

The strong performance of games alongside music and video highlights its central role in consumer entertainment budgets. The 2025 results underscore how the UK video game revenue 2025 story aligns with wider consumer demand for immersive and interactive media experiences.

Economic backdrop: GDP growth vs games revenue 2016–2025

From 2016 to 2025, the UK GDP rose by 12%, while games revenue expanded by 86%, meaning the games sector grew roughly 7.2 times faster than GDP over this period. This divergence illustrates the resilience and high growth potential of the UK video games market growth 2025 trajectory.

The long‑term momentum reflects ongoing innovation, strong consumer demand and effective monetisation across digital and hybrid formats. ERA CEO commentary and ERA UK data 2025 reinforce the sense that the industry is well positioned to sustain growth through 2026.

Top-selling titles and their impact on 2025 revenue (EA Sports FC 26)

EA Sports FC 26 was the year’s top seller, shifting over 1.97 million units across physical and digital formats. Such performance demonstrates the power of major, cross‑platform releases to lift overall digital game sales UK 2025 and anchor the year’s revenue mix.

This success also underscores how flagship titles can drive engagement and monetisation strategies within the UK video games market growth 2025, reinforcing the role of strong releases in sustaining momentum across both digital and boxed channels.

Outlook for 2026: momentum and expectations from ERA CEO Kim Bayley

ERA CEO Kim Bayley has expressed strong optimism that the momentum seen in 2025 will continue into 2026, pointing to ongoing innovation in gameplay formats, monetisation models and distribution strategies.

With continued growth in mobile and digital sales, alongside stable console downloads and a resilient ownership market, the UK video games market growth 2025 provides a solid foundation for further expansion in 2026, according to ERA’s outlook.

Frequently Asked Questions

What was the UK video game revenue 2025, and what drove the growth?

UK video game revenue 2025 reached £5.4 billion, up 7.4% year on year. Growth was led by mobile titles, which rose 8.8% to £1.88 billion and accounted for 35.5% of total games revenue, with digital sales totaling £5 billion (+8%). ERA data from NielsenIQ/GfK Entertainment, Omdia and GSD/IFSE underpin these figures.

How did mobile game revenue UK 2025 perform and what share of the market did it secure?

Mobile game revenue UK 2025 grew by 8.8% to £1.88 billion, representing 35.5% of total UK games revenue.

What does digital game sales UK 2025 look like according to ERA UK games data 2025?

Digital game sales UK 2025 amounted to £5 billion, an 8% year-on-year rise.

According to ERA UK games data 2025, which title led UK game sales?

EA Sports FC 26 was the biggest seller, shifting over 1.97 million units across physical and digital formats.

What does ERA UK games data 2025 reveal about ownership versus subscriptions in game revenue?

ERA UK games data 2025 shows that 45% of game revenue came from consumers buying games rather than subscribing.

How does the 2025 UK video games market growth compare to the wider entertainment sector, per ERA UK games data 2025?

In 2025, total UK entertainment (games, music and video) reached £13.3 billion, up 7.1% year on year. The games sector has risen 86% since 2016, reinforcing momentum into 2026.

| Category | 2025 figure | Key points |

|---|---|---|

| Total UK consumer spend on video games (2025) | £5.4 billion | Era citing NielsenIQ/GfK Entertainment, Omdia and GSD/IFSE; +7.4% YoY; largest rise since 2020. |

| YoY change | +7.4% | Demonstrates continued growth; pandemic year 2020 saw a 27.9% spike. |

| Mobile titles revenue | £1.88 billion | Up 8.8% YoY; mobile accounts for 35.5% of total game revenue. |

| Mobile share of total | 35.5% | Mobile revenue is a major driver of 2025 growth. |

| Console game downloads | $857.6 million | Up 11.5% YoY; growth in downloadable console games. |

| Physical sales | £318.8 million | Down 1% YoY; boxed sales represent 5% of total revenue. |

| Boxed sales share | 5% of total UK games revenue | Physical and boxed products still a small portion of the market. |

| Digital sales | £5 billion | Up 8% YoY; major component of revenue. |

| Top seller | EA Sports FC 26 (1.97 million units) | Led sales across physical and digital formats. |

| Ownership vs subscription | 45% of game revenue from buying vs subscribing | Compared with 16.6% (music) and 7.2% (video) for ownership share in those markets. |

| Economic context | GDP +12% (2016–2025); games revenue +86% | Games growth outpaces GDP growth, ~7.2x higher since 2016. |

| Growth trajectory | Momentum into 2026 | Growth slowed after 2020 pandemic spike but rebounded in 2025. |

| Entertainment market context | £13.3 billion (UK entertainment: games, music, video) | +7.1% YoY across all entertainment segments in 2025. |

Summary

Conclusion: UK video games market growth 2025 shows strong momentum across digital and mobile channels, with digital sales and mobile revenue driving most of the expansion, while boxed/physical share remains a small portion of total revenue. The market also benefits from a high ownership bias (45% revenue from buying vs subscribing) and a robust wider UK entertainment context, highlighting resilience and growth potential into 2026.